WEALTH MANAGERS

Wealth managers are the institutions whose advisory responsibilities make AI control a categorical, not optional, requirement. They are not merely intermediaries between products and clients; they are the entities entrusted with guiding individuals, families, and institutions through decisions that shape long-term financial outcomes. As AI becomes woven into planning, research, and client engagement, control becomes inseparable from fiduciary judgment and trust. In the final analysis, the future of wealth management will depend not simply on access to intelligent systems, but on the ability to govern them in service of the clients whose interests wealth managers are entrusted to protect.

FROM THE 2026 ANNUAL REPORT · SECTOR SUMMARY

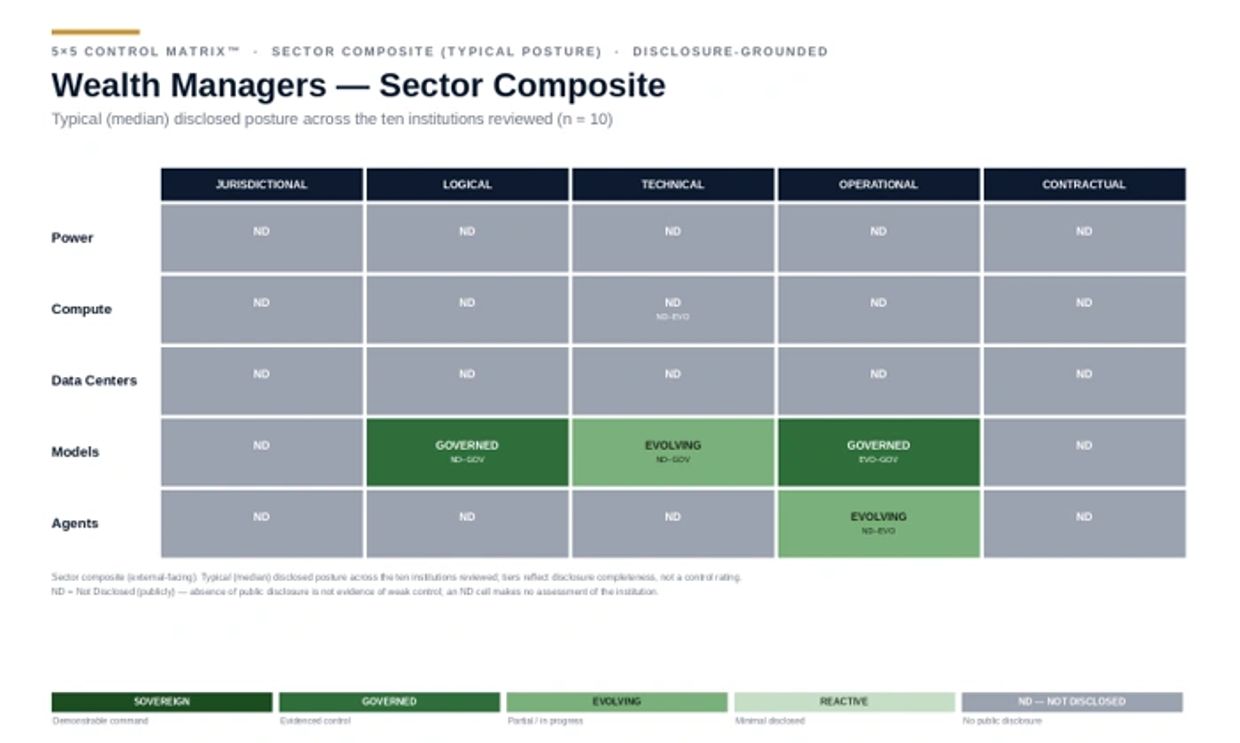

What the WEALTH MANAGERS sector shows

Wealth managers reach an evidenced-control standard on the model layer at the typical level, on both the logical and operational dimensions. A notable feature of the category is inheritance: several wealth arms operate under the disclosed control mechanisms of a banking parent, and the synthesis treats that inherited control consistently with the parent's. The sector's leading edge discloses named evaluation-and-deployment gates; its agentic operation, as in adjacent sectors, is disclosed at an evolving stage rather than in governed production, with at least one prominent advisor-facing agent disclosed as being in pilot rather than full deployment.

Heat-map classifications reflect publicly available information reviewed under the methodology described in this report. They are not assessments or certifications of any institution’s actual internal AI capabilities or controls. Grey (Not Disclosed) indicates the absence of public disclosure, not the absence of control.

The report does not evaluate, rate, certify, or benchmark any individual institution; the tiers reflect the completeness of public disclosure as our review found it, not an assessment of any institution's actual controls.

EXECUTIVE OVERVIEW

The AI Control Assessment for Wealth Management measures the institution's verified ability to own, govern, and audit the AI systems that process client financial profiles, generate financial plans, assess suitability, and produce client-facing recommendations and communications.

The assessment produces a 5×5 matrix of 25 specific, answerable governance questions. Each cell scored 1 (Reactive) to 4 (Sovereign), with maximum 100 total points, produces a control profile revealing not just the institution's overall governance posture, but exactly which infrastructure-governance intersections are exposed.

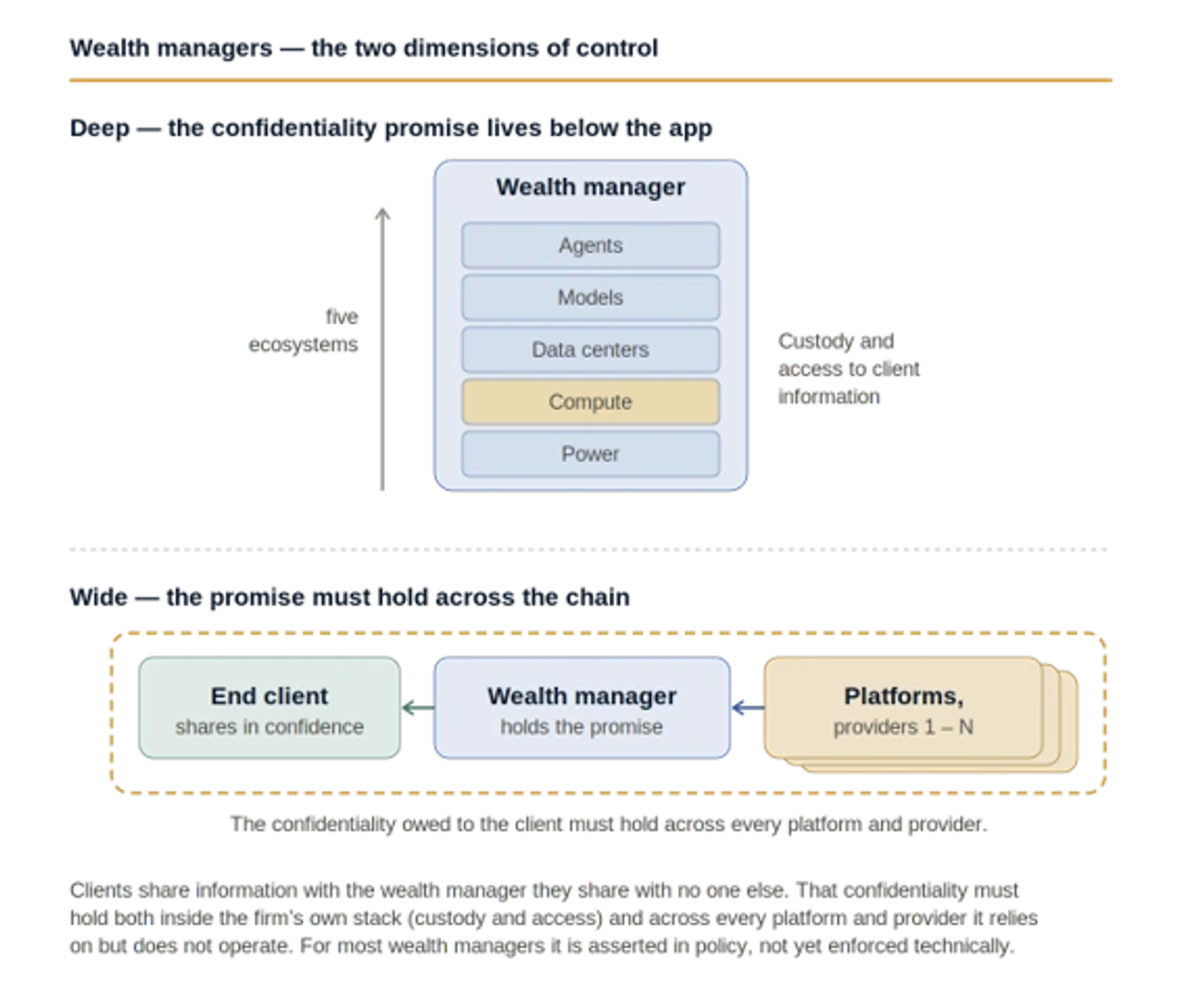

For wealth managers, exposure across the matrix is not just regulatory risk. It is fiduciary risk — the AI systems processing client information may operate under terms that contradict the confidentiality obligation the wealth management relationship promises.

THE WEALTH MANAGEMENT AI CONTROL CHALLENGE

Global Private Banks and Wirehouses

Their Mandate: Deliver comprehensive wealth management to ultra-high-net-worth and high-net-worth clients across investment management, financial planning, credit, and banking — with the discretion and accountability those relationships demand.

Core Challenges:

- Client data sovereignty across jurisdictions → Private banking clients hold assets across multiple jurisdictions. AI processing of those clients' comprehensive financial profiles creates data residency obligations under GDPR for EU clients, CCPA and state privacy laws for US clients, and applicable cross-border transfer restrictions — simultaneously. Standard API terms do not address any of them.

- Fiduciary AI explainability → SEC fiduciary standards for registered investment advisers extend to AI-assisted investment recommendations. MiFID II suitability and appropriateness requirements apply to AI-influenced advisory for EU clients. AI-generated financial plans, suitability assessments, and investment recommendations carry the same standard as human advice. Most private bank AI systems cannot produce the decision provenance records that standard requires.

- Ultra-high-net-worth client expectations → The most sophisticated and valuable wealth management clients are becoming aware of AI governance risks. The first private bank that can demonstrate technical protection of client financial information — not just contractual promises — will have a meaningful differentiator in a market where every firm claims client confidentiality.

Registered Investment Advisers (RIAs)

Their Mandate: Provide fiduciary investment advice to clients under SEC registration, with the care, skill, prudence, and diligence that standard requires — extended now to every AI system contributing to advisory decisions.

Core Challenges:

- SEC examination readiness → The SEC's examination division is developing focus on AI use in investment advisory. Early questions have addressed AI disclosure in Form ADV and marketing materials. The next wave will examine the AI systems generating suitability assessments, financial plans, and client recommendations — specifically whether those systems produce audit trails sufficient to demonstrate fiduciary compliance. RIAs without documented AI governance frameworks will be materially unprepared.

- Regulation Best Interest compliance → For dual-registrant RIA/broker-dealer firms, Reg BI's care, conflict, and disclosure obligations apply to AI-assisted investment recommendations. AI systems generating product recommendations must satisfy the best interest standard. The supervisory system requirements that FINRA imposes extend to AI-generated client communications and recommendations.

- Smaller compliance teams, identical obligations → Boutique RIAs face identical SEC fiduciary obligations to the largest wirehouses — with a fraction of the compliance resources. AI tools that create governance obligations their teams cannot manage represent risk that accumulates silently until an examination surfaces it.

Independent Financial Advisers and Broker-Dealers

Their Mandate: Serve retail and mass-affluent clients with investment guidance, financial planning, and product recommendations — under FINRA supervision requirements and the suitability and best interest standards that govern every client interaction.

Core Challenges:

- FINRA supervision extended to AI → FINRA supervisory system requirements extend to AI systems generating client recommendations and communications. FINRA's 2025 examination priorities explicitly included AI supervision as a focus area. AI-generated suitability assessments and client communications that cannot be supervised are advice that cannot be delivered compliantly.

- Platform AI governance gap → Most independent advisers and broker-dealers rely on platform providers for AI tools. The AI governance of those platforms is often opaque — the adviser's fiduciary and suitability obligations do not transfer to the platform. When a regulator examines the adviser's AI use, the answer "my platform handles it" is not a defensible response.

- Client data held by multiple providers → Independent advisers often use multiple technology providers — CRM, financial planning, portfolio management, AI tools — each with different data handling terms. The combination creates a patchwork of data governance that no single provider's terms address and that most advisers have never mapped against their regulatory obligations.

Multi-Family Offices

Their Mandate: Serve complex multi-generational family relationships with integrated investment management, financial planning, estate and tax advice, and family governance — with the deepest client relationships and the most sensitive information in wealth management.

Core Challenges:

- Intergenerational information sensitivity → Multi-family offices hold information about family structures, relationship dynamics, estate intentions, beneficiary conflicts, and succession plans that is extraordinarily sensitive — affecting not just the primary client but their families across generations. AI processing of this information under standard terms creates exposure that extends far beyond standard privacy frameworks.

- Bespoke mandate complexity → Family offices manage investment mandates of exceptional complexity — customised investment policies, values-based restrictions, family governance requirements, and liquidity needs that differ by family member and generation. AI-assisted portfolio management that cannot demonstrate mandate compliance at the family-specific level creates client relationship risk that standard suitability monitoring does not address.

- Absence of formal regulatory framework → Single-family offices often fall outside formal SEC registration thresholds. Multi-family offices are regulated at varying levels. The absence of a prescriptive regulatory framework does not remove the fiduciary obligation — it places greater weight on the institution's own governance standards, including the standards applied to AI.

WEALTH MANAGERS — AI USE CASES

CLIENT INTELLIGENCE & PERSONALIZATION

From relationship management → genuinely personal advisory

Use Cases

- AI-driven client profiling across financial, behavioral, and life-stage dimensions

- Goal-based planning intelligence with dynamic scenario modeling

- Life event detection and proactive advisory triggers

- Holistic household wealth analysis across all assets and liabilities

Value Creation

- Deeper, more durable client relationships

- Proactive advisory that clients experience as genuinely personal

- Increased wallet share through comprehensive financial visibility

Governance Reality Check

Client profiling AI processes the most sensitive information your clients possess — estate structures, family dynamics, health conditions, relationship status. That data submitted to an external AI model is processed on provider infrastructure under terms that most wealth management legal teams have not reviewed against their fiduciary obligations. Client intelligence is only sovereign if the governance enforces it.

Tie to Stack

- Models + Data Centers → governed client intelligence under strict data sovereignty

- OLTAIX™ → ensures every client insight is traceable, consistent, and suitability-aligned

PORTFOLIO MANAGEMENT & SUITABILITY

Every portfolio aligned to every mandate — always

Use Cases

- AI-driven suitability monitoring across all client portfolios

- Automated rebalancing with mandate alignment verification

- Tax-loss harvesting intelligence at client and household level

- Direct indexing optimization under fiduciary constraints

Value Creation

- Continuous suitability compliance without manual monitoring burden

- Consistent application of investment mandates across all client tiers

- Demonstrable fiduciary governance for regulatory and client purposes

Governance Reality Check

Continuous suitability monitoring is only meaningful if the AI performing it produces institution-controlled audit records. Suitability AI that monitors without logging — in your systems, accessible to you and your regulators — is monitoring that cannot be demonstrated. Demonstrated compliance is not the same as assumed compliance.

Tie to Stack

- Models → suitability and mandate intelligence with complete decision provenance

- OLTAIX™ → real-time compliance enforcement with full audit trail on every portfolio decision

FINANCIAL PLANNING & SCENARIO INTELLIGENCE

Plan for the futures that matter — including the ones clients fear

Use Cases

- AI-driven financial planning with multi-scenario modeling

- Retirement readiness intelligence with dynamic projection

- Estate and tax planning intelligence across complex household structures

- Insurance gap analysis and protection planning

Value Creation

- More confident client conversations grounded in evidence

- Differentiated planning capability as a competitive advantage

- Stronger client retention through forward-looking advisory

Governance Reality Check

Financial plans generated by AI that inform client investment decisions carry the same fiduciary standard as human-generated plans. When a plan is based on incorrect assumptions or produces outputs that do not reflect the client's actual circumstances, the AI system's role in that failure must be reconstructable from audit records. Most wealth management AI planning systems do not produce those records.

Tie to Stack

- Models + Agentic Applications → governed planning intelligence with full scenario provenance

- OLTAIX™ → audit trail on every planning recommendation and scenario output

ADVISOR PRODUCTIVITY & INTELLIGENCE

Give every advisor the capabilities of an entire research team

Use Cases

- AI-driven meeting preparation with client intelligence briefs

- Automated portfolio commentary and client communication drafting

- Next-best-action intelligence for advisor-client engagement

- Prospect intelligence and pipeline prioritization

Value Creation

- Dramatic increase in advisor capacity for high-value client interactions

- More consistent client experience across all advisor tiers

- Reduced time on administrative and reporting tasks

Industry Signal

SEC Marketing Rule requirements apply to AI-generated client communications that reference performance or make investment claims. FINRA supervisory requirements extend to AI systems generating client-facing content. AI-generated advisor communications that cannot be supervised under applicable standards are communications that cannot be sent compliantly.

Tie to Stack

- Agentic Applications → advisor copilots operating under compliance guardrails

- OLTAIX™ → ensures every advisor output is compliant, consistent, and explainable

COMPLIANCE & REGULATORY GOVERNANCE

Every recommendation defensible — before and after the fact

Use Cases

- Real-time suitability monitoring across all client activity

- Automated KYC/AML intelligence and alert management

- Surveillance and conduct risk monitoring across advisor activity

- Regulatory examination readiness with on-demand audit trail construction

Value Creation

- Reduced compliance risk across the advisory operation

- Faster, more accurate regulatory responses

- Institutional-grade governance posture for examination and client scrutiny

Industry Signal

The SEC's examination focus on AI in wealth management is intensifying. Early examinations have addressed AI disclosure in Form ADV. The next wave will examine AI systems generating suitability assessments and financial plans. Wealth managers with documented AI governance frameworks will be materially better positioned than those building it in response to examination findings.

Tie to Stack

- Models + OLTAIX™ → governed compliance intelligence with real-time policy enforcement

- Data Centers → client data sovereignty and jurisdictional compliance

CLIENT REPORTING & TRANSPARENCY

Reporting that builds trust, not just informs

Use Cases

- AI-generated client reports with plain-language performance explanation

- Real-time portfolio transparency and look-through analytics

- ESG reporting and impact measurement for values-aligned clients

- Personalized market commentary aligned to each client's portfolio and goals

Value Creation

- Stronger client trust through proactive, explainable communication

- Differentiated reporting as a retention and acquisition tool

- Reduced cost of report production across all client tiers

Industry Signal

Sophisticated wealth management clients are beginning to ask what AI systems processed their information, how it was used, and how it was protected. The wealth manager that proactively demonstrates AI governance transparency — rather than responding to client questions about it — is building trust that is increasingly difficult for competitors to replicate.

Tie to Stack

- Agentic Applications → governed report generation at scale

- OLTAIX™ → data integrity and consistency across every client-facing output

REQUEST The State of AI Control in Institutional Finance

AVAILABLE ON A RELATIONSHIP BASIS TO QUALIFYING INSTITUTIONS

All discussions covered under NDA. Tiers reflect public-disclosure completeness, not assessments of any institution's actual controls.

AI is a given. Control is not.™