FROM THE 2026 ANNUAL REPORT · SECTOR SUMMARY

What the RETIREMENT/TPA sector shows

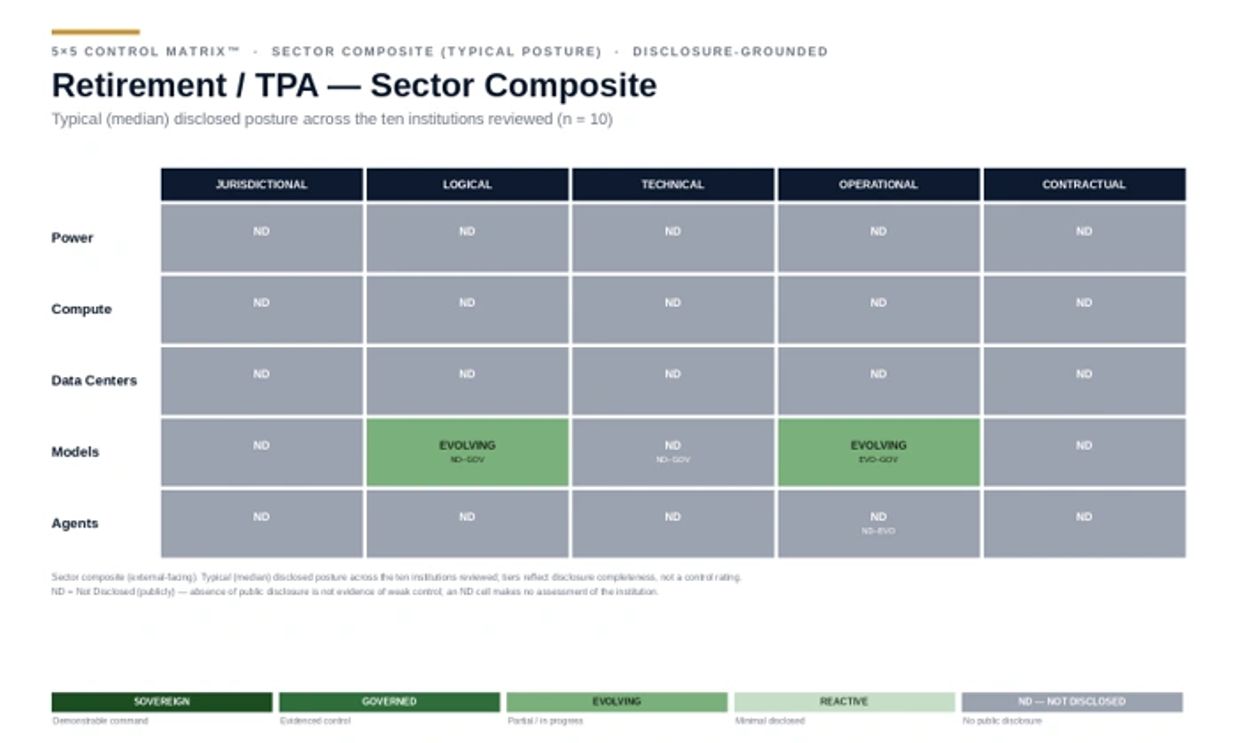

Retirement and third-party administration providers sit at an evolving posture on the model layer at the typical level, on both the logical and operational dimensions, with the strongest firms in the category reaching evidenced control through named, full-lifecycle governance frameworks and deployed governance tooling. The range is meaningful: several providers inherit disclosed control from an affiliated asset manager or recordkeeping parent, while others disclose stated governance without a corresponding auditable mechanism. The sector's leaders increasingly disclose the kind of intake-to-monitoring framework that distinguishes evidenced control from stated intent.

Heat-map classifications reflect publicly available information reviewed under the methodology described in this report. They are not assessments or certifications of any institution’s actual internal AI capabilities or controls. Grey (Not Disclosed) indicates the absence of public disclosure, not the absence of control.

The report does not evaluate, rate, certify, or benchmark any individual institution; the tiers reflect the completeness of public disclosure as our review found it, not an assessment of any institution's actual controls.

THE STEWARDS OF AMERICAN RETIREMENT SECURITY

Retirement Plan Recordkeepers

Their Mandate:Administer defined contribution retirement plans for millions of participants with accuracy, security, and fiduciary discipline.

Core Challenges:

- ERISA Fiduciary Exposure → AI systems performing compliance testing, retirement income projections, and benefit determinations carry ERISA's full fiduciary standard to every technology layer running them.

- Participant Data Sensitivity → Social Security numbers, beneficiary designations, and hardship documentation represent the most sensitive personal financial data in the US financial system.

- DOL Examination Readiness → ERISA Section 504 grants the DOL authority to demand any records related to plan administration — including AI system logs that most providers do not hold in institution-controlled systems.

- SECURE 2.0 Obligations → New provisions for retirement income projections, emergency savings, and auto-portability create expanded AI use cases, each carrying ERISA's fiduciary standard.

Third Party Administrators (TPAs)

Their Mandate:Perform plan administration functions — compliance testing, recordkeeping, participant communication, and benefit processing — for plan sponsors who cannot satisfy ERISA obligations independently.

Core Challenges:

- Dual Accountability → TPAs are accountable to plan sponsors as fiduciaries and to participants as the ultimate beneficiaries of every plan administration decision made on their behalf.

- Compliance Testing Accuracy → AI-driven ADP/ACP, top-heavy, and coverage testing must produce results sufficient for IRS examination. Errors leading to plan disqualification create tax consequences for plan sponsors and participants alike.

- Contractual Exposure → Standard model API terms do not provide the audit rights, participant data protections, or Section 408(b)(2) passthrough rights that ERISA's service provider framework requires.

- Agent Governance Gap → Autonomous agents processing enrollments, loans, distributions, and hardship withdrawals perform ERISA plan administration functions — without the audit trails ERISA requires for those functions.

Insurance Company Retirement Platforms

Their Mandate:Deliver defined contribution, annuity, and insurance-wrapped retirement products under both ERISA and state insurance regulatory frameworks simultaneously.

Core Challenges:

- Dual Regulatory Overlay → AI governance must satisfy ERISA's fiduciary standard and state insurance AI regulations simultaneously — two frameworks that were not designed with each other in mind.

- Retirement Income AI → AI systems generating annuity illustrations, income projections, and in-force management recommendations carry both SEC registration obligations for variable products and ERISA fiduciary obligations for plan participants.

- Data Sovereignty Across Custodians → Insurance platforms aggregate participant data across multiple custodians, investment managers, and actuarial systems — creating cross-ecosystem governance complexity that no single provider's standard terms address.

- PTE 2020-02 Compliance → AI-driven investment recommendations to retirement plan participants must satisfy DOL's prohibited transaction exemption — a standard that most AI vendor agreements were not written to support.

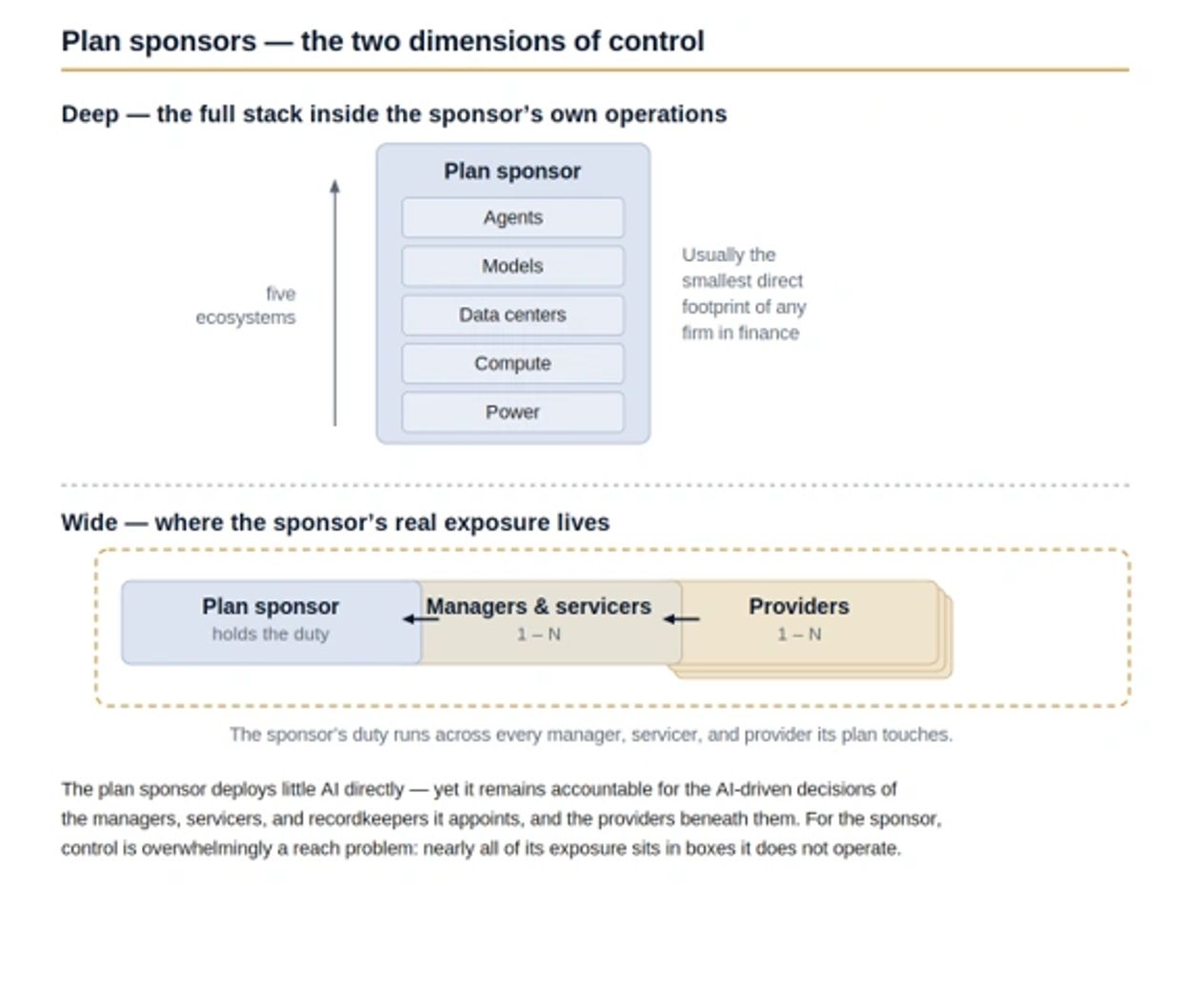

Government and Non-Profit Plan Administrators

Their Mandate:Administer 401(k), 403(b), 457, and governmental retirement plans for public sector and non-profit employees under a patchwork of ERISA, IRS, and state regulatory requirements.

Core Challenges:

- Regulatory Complexity → Government plans face IRS qualification requirements, state pension law, and in some cases ERISA-equivalent state fiduciary standards — each with different implications for AI governance.

- Budget Constraints → Limited technology budgets relative to private sector peers create governance gaps that AI adoption is accelerating rather than closing.

- Participant Vulnerability → Public sector and non-profit participants often have limited financial sophistication and fewer alternative retirement savings options — making the accuracy of AI-driven retirement income projections and enrollment guidance especially consequential.

- Audit Exposure → Government plan audits by state comptrollers, inspector generals, and legislative audit bodies create AI governance documentation requirements that standard commercial platform terms do not satisfy.

RETIREMENT PLAN PROVIDERS — AI USE CASES

PLAN COMPLIANCE TESTING & QUALIFICATION

"From manual calculation → AI-driven defensibility"

Use Cases

- AI-driven ADP/ACP, top-heavy, and coverage testing at scale

- Automated correction identification and remediation recommendations

- Real-time compliance monitoring across plan populations

- IRS audit trail generation with cryptographic integrity verification

Value Creation

- Elimination of manual testing errors and plan disqualification risk

- Faster testing cycles — weeks to days

- IRS examination readiness on demand

- Reduced cost of compliance for plan sponsors

ERISA Reality Check

- AI compliance determinations carry identical audit trail requirements to human calculations. Errors due to model drift that go undetected until IRS examination create tax penalties for plan sponsors and participants alike.

Tie to Stack

- Models + Data (Intelligence Layer) → compliance determination engines with validated, auditable outputs

- OLTAIX™ → governs model behavior, flags drift, produces immutable compliance records for DOL and IRS examination

RETIREMENT INCOME PROJECTION & PLANNING

"From static projections → personalized, SECURE 2.0-compliant intelligence"

Use Cases

- AI-generated retirement income projections satisfying SECURE 2.0 benefit statement requirements

- Personalized savings rate optimization and gap analysis at participant level

- Decumulation modeling and withdrawal sequencing recommendations

- Monte Carlo simulation at scale across plan populations

Value Creation

- SECURE 2.0 compliance without manual calculation overhead

- Improved participant retirement readiness outcomes

- Plan sponsor differentiation through participant-level intelligence

- Reduced liability from projection inaccuracy

Industry Signal

- DOL is developing examination focus on the accuracy and governance of AI-generated retirement income projections. Providers deploying projection AI without real-time model monitoring are accumulating examination exposure.

Tie to Stack

- Models → retirement income projection engines with participant-specific context

- OLTAIX™ Control Tower → monitors projection accuracy, detects model drift, maintains audit trails for every projection delivered

PARTICIPANT ENGAGEMENT & FINANCIAL WELLNESS

"From mass communication → governed behavioral intelligence"

Use Cases

- AI-driven personalized participant communication at scale

- Behavioral nudge engines for enrollment, contribution escalation, and investment selection

- Financial wellness assessments and personalized action plans

- Multilingual participant support through governed AI agents

Value Creation

- Higher enrollment rates and participant savings outcomes

- Reduced call center volume through intelligent self-service

- Plan sponsor retention through demonstrable participant outcomes

- Scalable personalization without proportional staffing cost

ERISA Reality Check

- AI systems influencing participant investment decisions must navigate ERISA's prohibited transaction rules. The distinction between financial wellness education and individualized investment advice is legally significant — and AI governance frameworks must enforce it technically, not only by policy.

Tie to Stack

- Apps (Agentic) → participant engagement agents with ERISA-compliant guardrails

- OLTAIX™ → enforces education vs advice boundaries, logs every participant interaction for DOL examination readiness

MANAGED ACCOUNTS & INVESTMENT GUIDANCE

"From generic defaults → fiduciary-grade personalized investment"

Use Cases

- AI-driven managed account portfolio construction at participant level

- Investment menu optimization and QDIA governance

- PTE 2020-02 compliant AI investment advice infrastructure

- Suitability monitoring and conflict-of-interest detection

Value Creation

- Participant-level investment personalization at scale

- Demonstrable fiduciary compliance for plan sponsors

- Improved retirement outcomes through individually optimized portfolios

- Reduced prohibited transaction exposure under DOL exemption frameworks

Industry Signal

- The DOL's developing fiduciary rule guidance has direct implications for AI-driven investment recommendations in retirement plans. Providers deploying managed account AI without PTE 2020-02 compliant governance frameworks are creating fiduciary exposure for themselves and their plan sponsor clients simultaneously.

Tie to Stack

- Models → participant-level portfolio construction with evidence-based recommendations

- OLTAIX™ → governs fiduciary compliance, maintains recommendation audit trails, enforces conflict-of-interest controls

PLAN ADMINISTRATION & AUTONOMOUS PROCESSING

"From manual transactions → governed agentic administration"

Use Cases

- Autonomous enrollment processing and auto-feature administration under SECURE 2.0

- AI-driven loan origination, hardship withdrawal review, and distribution processing

- Beneficiary administration and QDRO processing with automated eligibility verification

- Form 5500 and regulatory filing preparation with AI-assisted accuracy verification

Value Creation

- Dramatic reduction in manual processing costs and error rates

- Faster participant transaction completion — hours to minutes

- ERISA-defensible documentation for every automated decision

- Plan sponsor confidence through transparent, auditable automation

ERISA Reality Check

- Every autonomous agent processing participant enrollments, loans, distributions, and hardship withdrawals is performing a plan administration function subject to ERISA. The record-keeping requirements, audit trail obligations, and fiduciary accountability that attach to those functions attach with equal force to the agents performing them. Most retirement services agent deployments cannot produce the complete, immutable action records ERISA requires.

Tie to Stack

- Apps (Agentic) → plan administration agents with complete action logging and human oversight checkpoints

- OLTAIX™ → enforces ERISA documentation requirements, logs every agent action in institution-controlled systems accessible to plan sponsors and DOL examiners

PLAN SPONSOR REPORTING & RELATIONSHIP INTELLIGENCE

"From periodic reporting → real-time fiduciary transparency"

Use Cases

- AI-generated plan sponsor dashboards — performance, participant outcomes, compliance status

- Automated 408(b)(2) fee disclosure preparation and accuracy verification

- Benchmarking intelligence — plan design, fee competitiveness, participant outcomes

- Predictive plan sponsor retention modeling and relationship health scoring

Value Creation

- Stronger plan sponsor trust through real-time transparency

- Reduced cost of regulatory reporting and disclosure preparation

- Proactive identification of plan sponsor relationship risk before mandate loss

- Competitive differentiation through governance transparency as a service

Industry Signal

- Large plan sponsors conducting AI governance due diligence are beginning to require that service providers demonstrate matrix-level governance across their AI stack. The first retirement plan provider to offer real-time AI governance transparency to plan sponsors as a standard service will set the market standard that others must match.

Tie to Stack

- Apps (Agentic) → plan sponsor intelligence and reporting agents

- OLTAIX™ → ensures data integrity, consistency, and auditability across all plan sponsor-facing outputs

- Data → unified participant and plan data across all ecosystems for accurate, real-time reporting

THE COMPLIMENTARY ASSESSMENT OFFER

Designed specifically for retirement plan providers and TPAs.

The AI Control Assessment for Retirement Plan Providers is available at no cost to qualifying institutions.

Institutional AI offers complimentary assessments to retirement plan providers and TPAs in exchange for anonymized benchmark data that sharpens peer comparisons for everyone in the sector.

The institution receives a complete governance diagnostic — scored across 25 specific intersections of the 5×5 Control Matrix, benchmarked against peer institutions, and mapped to a strategic direction.

Institutional AI receives a real-world data point that makes the benchmarks more accurate for the next institution that takes the assessment.

No engagement required. No obligation. No sales process until the institution decides one is warranted.

REQUEST The State of AI Control in Institutional Finance

available on a relationship basis to qualifying institutions

All discussions covered under NDA. Tiers reflect public-disclosure completeness, not assessments of any institution's actual controls.

AI is a given. Control is not.™